But that might increase Fed authorities' issues about a market bubble that eventually pops, Bostjancic says." it's a close call," Bostjancic states. She, in addition to economic experts at Goldman and JPMorgan Chase, anticipate the Fed to shift the bond purchases to trim rates while Nomura, Barclays and Morgan Stanley predict the Fed will stand pat.

Rates are currently traditionally low and the real estate market is growing. A shift in the Fed's mix might push down home loan rates by about 15 basis points, reducing the monthly payment on a $200,000 home loan by $15, or $180 year, says Tendayi Kapfidze, primary economist of Providing Tree. Many economists are more positive the Fed will provide more specific guidance on how low long it will continue to purchase bonds.

Goldman Sachs believes the Fed will say it will keep buying bonds at the current speed till the labor market is "on track" to reach full employment and inflation is "on track" to reach 2%. That resembles the Fed's requirements for raising its key short-term rate but not as stiff.

Bostjancic states Fed authorities most likely wish to prevent another "taper temper tantrum" a 2013 spike in Treasury yields when Fed authorities unexpectedly indicated they would begin winding down bond purchases following the Terrific Recession of 2007-09. Also, financiers now expect the Fed to begin tapering the bond purchases in late 2021 or early 2022.

Alexander, however, states the Fed might wait till the outlook is clearer prior to fine-tuning its assistance. In September, the Fed forecasted the economy would contract 3. 7% this year and joblessness would end the year at 7. 6%. But the economy has recuperated from the pandemic more swiftly than anticipated, with joblessness already at 6.

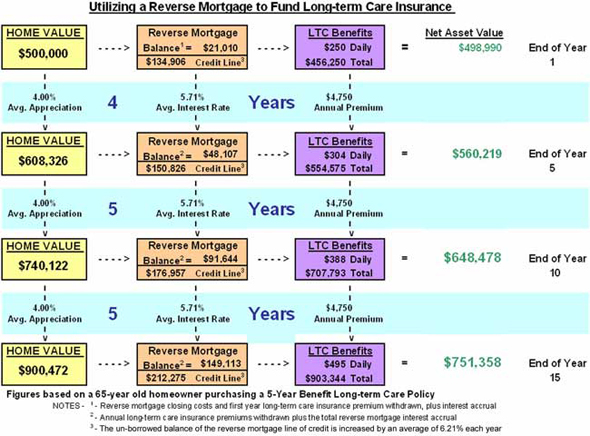

More About What Are Reverse Mortgages And How Do They Work

Goldman Sachs expects the Fed to modify its forecast to a 2. 5% contraction this year and joblessness of 6. 8% at year-end. Goldman likewise anticipates the Fed to decently raise its estimate of financial growth next year to 4. 2%, up from its previous forecast of 4%. Oxford, nevertheless, reckons the Fed will lower its estimate for next year as the results of the infection spike surpass the increase from the vaccine.

Shopping around for a mortgage or home mortgage will assist you get the very best financing deal. A mortgage whether it's a home purchase, a refinancing, or a home equity loan is an item, similar to a cars and truck, so the price and terms might be negotiable. You'll desire to compare all the costs involved in obtaining a mortgage.

Obtain Information from Numerous Lenders Obtain Very important Expense Information Mortgage are available from several types of lending institutions thrift institutions, business banks, mortgage companies, and cooperative credit union. Various lending institutions may quote you different rates, so you should get in touch with numerous lenders to ensure you're getting the best cost. You can likewise get a mortgage through a home loan broker.

A broker's access to a number of lenders can imply a broader selection of loan products and terms from which you can pick. Brokers will typically get in touch with several lending institutions concerning your application, however they are not obligated to find the finest deal for you unless they have actually contracted with you to serve as your representative.

Whether you are dealing with a lender or a broker may not constantly be clear. Some monetary institutions run as both lending institutions and brokers. And many brokers' advertisements do not utilize the word "broker." Therefore, make certain to ask whether a broker is involved. This information is very important because brokers are normally paid a cost for their services that may be separate from and in addition to the loan provider's origination or other costs.

Excitement About How To Calculate Interest Only Mortgages

You ought to ask each broker you work with how she or he will be compensated so that you can compare the different costs. Be prepared to negotiate with the brokers along with the lenders. Make sure to get info about home mortgages from several loan providers or brokers. Know just how much of a down payment you can afford, and find out all the costs involved in the loan.

Request details about the very same loan amount, loan term, and kind of loan so that you can compare the details. The following details is essential to obtain from each lender and broker: Ask each loan provider and broker for a list of its existing home loan interest rates and whether the rates being priced estimate are the most affordable for that day or week.

Keep in mind that when rates of interest for adjustable-rate mortgages increase, generally so do the regular monthly payments. If the rate priced quote is for an adjustable-rate mortgage, ask how your rate and loan payment will differ, consisting of whether your loan payment will be reduced when rates decrease. Inquire about the loan's yearly portion rate (APR).

Points are fees paid to the lender or broker for the loan and are typically connected to the interest rate; normally the more points you pay, the lower the rate. Check your regional paper for info about rates and points presently being offered. Request points to be estimated to you as a dollar quantity rather than just as the number of points so that you will know just how much you will really https://plattevalley.newschannelnebraska.com/story/43143561/wesley-financial-group-responds-to-legitimacy-accusations need to pay.

Every lender or broker ought to be able to offer you a quote of its costs. Many of these costs are flexible. Some charges are paid when you use for a loan (such as application and appraisal costs), and others are paid at closing. Sometimes, you can obtain the cash needed to pay these charges, but doing so will increase your loan quantity and total expenses.

The smart Trick of What Is The Interest Rate Today For Mortgages That Nobody is Talking About

Ask what each charge consists of. A number of products may be lumped into one cost. Request for an explanation of any charge you do not comprehend. Some typical costs associated with a home mortgage closing are listed on the Home loan Shopping Worksheet. Some lenders require 20 percent of the home's purchase price as a down payment.

If a 20 percent deposit is not made, lending institutions typically require the homebuyer topurchase private home loan insurance coverage (PMI) to safeguard the loan provider in case the homebuyer fails to pay. When government-assisted programs like FHA ( Federal Real Estate Administration), VA (Veterans Administration), or Rural Development Services are readily available, the down payment requirements may be substantially smaller.

Ask your lender about unique programs it may use. If PMI is required for your loan Ask what the total cost of the insurance coverage will be. Ask how much your monthly payment will be when the PMI premium is included. Once you know what each lending institution needs to provide, work out the very best offer that you can. how to qualify for two mortgages.

The most likely reason for this difference in price is that loan officers and brokers are typically permitted to keep some or all of this difference as https://panhandle.newschannelnebraska.com/story/43143561/wesley-financial-group-responds-to-legitimacy-accusations extra payment. Normally, the distinction in between the most affordable readily available price for a loan product and any higher rate that the customer agrees to pay is an excess.